Newsletter 2016 – Company Highlight

– Event 1 –

Event Name: The Society of Chinese Accountants and Auditors – Beijing Visiting Mission

Location: Beijing, China

Date: 26th – 28th June 2016

We are much honored to be a delegate of the 2016 Beijing Visiting Mission, which organized by the Society of Chinese Accountants and Auditors (“SCAA”). Various senior Mainland officials were met to exchange views on the latest development and regulation of the nation, including Ministry of Finance (“MoF”), Chinese Institute of Certified Public Accountants (“CICPA”), the Audit office of the People’s Republic of China (“AOPRC”), the State Administration of Taxation (“SAT”), Beijing Institute of Certified Public Accountants (“BICPA”) and the National Equities Exchange and Quotations Center (“NEEQ”).

The delegation discussed various issues with the Mainland officials, for instances, CICPA highlighted their recent progress and policies in response to the tax challenges of the digital economy in Mainland; AOPRC shared the effectiveness to have a comprehensive audit trail and the focus of the AOPRC in 2016; the corresponding measures of the SAT in fighting tax evasion, identifying the tax residency, issues in double taxation and taxation honor system. Meanwhile, we exchanged our views and ideas during the meeting including hot topics like “Country by Country (CbC) Reporting” and “Base Erosion and Profits Shifting (BEPS) project.

We would like to express our gratitude to SCAA for organizing a successful trip. This was a valuable visit that we use to meet with various senior Mainland officials to obtain a deeper understanding of the Mainland recent development and exchange our feedbacks.

– Event 2 –

Event Name: Cross-Strait Four Regions – 2016 Tax Conference

Location: Hong Kong Convention and Exhibition Centre, Hong Kong

Date: 5th October 2016

Our managing director Ms. CY Chan was invited to attend the Cross- Strait Tax Conference 2016. Tax professions from Mainland China, Taiwan, Macau and Hong Kong and experts from respective jurisdictions shared their views and knowledges on (1) the recent development of digital economy and (2) the tax challenges of digital economy.

Our Hong Kong tax profession commented that digital economy has changed the general assumption on taxation of cross-border digital transactions , governments would therefore trying to reform their tax rules for a more effective tax collection mechanism to avoid from revenue loss. Taiwan tax profession mentioned it is difficult to apply existing tax rules on businesses in digital economy, but tax professionals need to work together to ensure that taxpayers in this economy pay the right amount of tax in the right jurisdiction. Macau tax profession said that the digital economy simplifies the global communication and it has significantly changed our modes of doing business and records keeping. With the digital evolution continues around the globe, the trend of paperless transactions and paperless reporting increase the difficulties for tax authorities in getting taxes from companies who operate in the digital economy. Therefore, changes were required to the existing international tax rules to overcome these challenges.

In the final report on Base Erosion and Profit Shifting (“BEPS”) Action Plan released by the Organisation for Economic Co-operation and Development (“OECD”), it has highlighted the existing tax rules designed exclusively for the digital economy would prove unworkable and propose specific tax rule changes. The tax conference provided a great platform for tax experts from the Mainland, Taiwan, Macau and Hong Kong to get update and exchange views on the issue of tax challenges of the digital economy. We have also shared our experiences and ideas on how to ensure an effective tax collection with respect to the cross-border supply of digital goods and services. It was a very informative and meaningful forum.

If you are interested to have a deeper understanding about the tax impact on your company, please feel free to contact us.

– Event 3 –

Event Name: AOTCA International Annual Tax Conference 2016

Location: Hong Kong Convention and Exhibition Centre, Hong Kong

Date: 6th – 7th October 2016

The 24th Asia-Oceania Tax Consultants’ Association (AOTCA) international annual tax conference was held in the Hong Kong Convention and Exhibition Center this year with over 300 tax professionals attending from across the industry.

AOTCA was founded in 1992 by a group of tax professionals and has expanded to include 20 leading organizations from 16 countries in Asia and Oceania. The association aims at promoting the exchange of information across all tax professionals and to discuss tax issues in the Asian-Pacific region.

Three key topics were presented in the last meeting: (1) Post BEPS, Opportunities and Challenges, (2) the update of BEPS, and (3) Country by Country (CbC) Reporting. In addition, tax profession and representative of business communities were invited to discuss “how do business perceive the current tax environment” and “will the BEPS recommendations achieve- fair taxation”.

The landscape of international taxation has completely changed, taxpayers should be well equipped themselves with contingency plans that can be applied under different circumstances. On the other hand, tax professionals cannot isolate themselves from the tax development in the outside world and are encouraged to broaden their views and keep their knowledge up to international standards, proactively provide advices to their client in order to assist the client’s global business development.

We are delighted to participate in the conference and we looking forward to the opportunity to share our professional insights, views, ideas and opinions in the next AOTCA annual conference.

Newsletter 2016 – Market Flash

– Global Tax Reform: BEPS and Business –

Background of Tax Reforms

Since G20 leaders decided to update international tax rules, countries started to implement Base Erosion and Profit Shifting (BEPS) project which released by the Organisation for Economic Co-operation and Development’s (OECD). The tax reforms put an end to any tax advantage companies receive by shifting their profits into tax havens and it close the opportunities that companies take benefits from agressive tax planning. Meanwhile, the BEPS reforms is likely to increase the tax burdens and uncertainty of the company’s tax exposure, companies that are prompt in preparing and make adjustments before the tax changes would help to shape a competitive advantage over competitors.

What is a BEPS project?

According to the interpretation of OECD, “BEPS project is a tax aviodance strategies that exploit gaps and mismatches in tax rules to artificially shift profits to low or no-tax locations. Under the inclusive framework, over 100 countries and jurisdictions are collaborating to implement the BEPS measures and tackle BEPS.”

How does it change the tax exposure and potential tax costs of a company?

Fact findings in 2016/ Impacts of BEPS

Evidence showed that there is a growing list of tax investigations and disputes between governmental authorities and MNEs over their offshore funds.

A report of Aaron Menderlson, ITEP interim published that:

Prominent Cases in 2016:

- EU investigators have examined how paid a tax rate of less than 1% on their European sales in last some years

- reached an agreement with UK government to pay additional £130 million in corporate tax and interest

- The group has been accused of evading taxes for at least €1 billion in Europe

Who will be the European Commission’s next target?

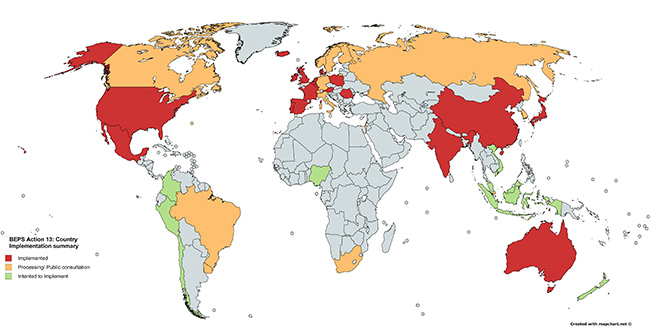

There are 15 Actions in the BEPS Project (see note 1), including digital economy, interest deductions, transfer pricing and disclosure of aggressive tax. Each jurisdiction is considering to implement the recommendations laid out in OECD’s final reports on BEPS action plan.

Country Focus on BEPS Actions

Note 1:

BEPS Profit- 15 Actions released by OECD

Action 1: Address the tax challenges of the digital economy;

Action 2: Neutralise the effects of hybrid mismatch arrangements

Action 3: Strengthen controlled foreign companies rules;

Action 4: Limit base erosion via interest deductions and other financial payments

Action 5: Counter harmful tax practices more effectively, taking into account transparency & substance

Action 6: Prevent treaty abuse;

Action 7: Prevent artificial avoidance of Permanent establishment (PE) status

Action 8, 9, 10: Assure that transfer pricing outcomes are in line with value creation;

Action 11: Establish methodologies to collect and analyze data on BEPS;

Action 12: Require taxpayers to disclose aggressive tax-planning arrangements;

Action 13: Re-examine transfer pricing documentation and institute Country by Country Reporting (“CbC Reporting”)

Action 14: Make dispute resolution mechanisms more effective; Action 15: Develop a multilateral instrument

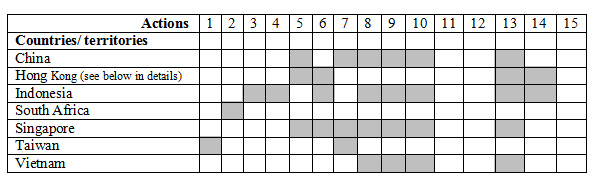

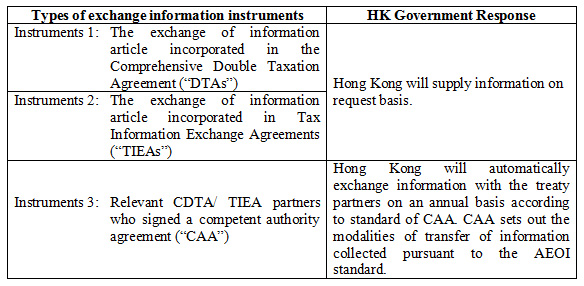

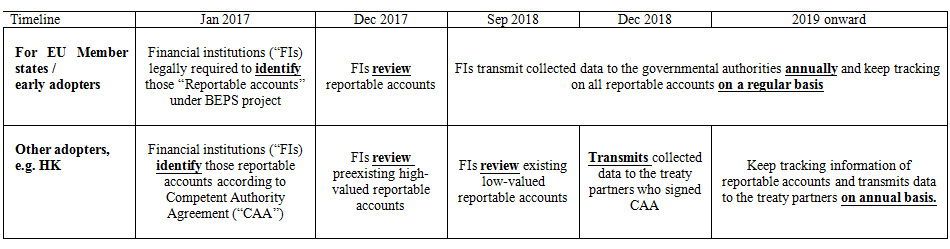

Hong Kong Actions in response to BEPS- Action 13

Under the current mechanism, HK has 3 types of exchange information instruments to supply information to treaty partners:

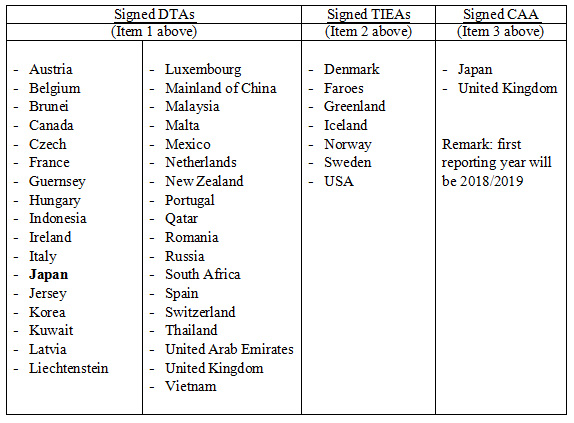

Hong Kong has signed with below countries/ territories:

Timetable dedicated by EU/ non-EU members

Information to be reported:

- Interests

- Dividends

- Account balance/ Account values

- Sales proceeds from financial assets, etc…

Case illustration

“BEPS [reform] significantly increases the likelihood that a company’s existing business model that was formerly not locally taxable becomes a taxable presence.” says Paul Griffiths of the EY Asia-Pacific Tax Center.

It was believed that the BEPS project is a business transformation issue rather than simply a global tax reform. How does it change the business practices? How does it change the tax exposure and potential tax costs of a company?

The examples below demonstrate the tax impact:

Tax exposure of ABC Trading Co. (“ABC”)

IN THE PAST:

- ABC was not liable to tax in Country A because there is no office, no personnel and no activity presence in Country A.

- In addition, ABC would not be locally taxable in UK/ PRC as there was no taxable presence.

NOW, under BEPS project:

- ABC is still not liable to tax in Country A because there are no office, no personnel and no activity presence in Country A. However, Country A will collect ABC’s financial information and subsequently provide to UK and PRC according to BEPS action 13- CbC Reporting.

- OECD redefines the meaning of tax presence. With activities which related to planning, procurement and service spectrum, ABC is now considered to have Permanent Establishment (“PE”) in UK and PRC and therefore having a taxable presence.

- With the reason in point 2, UK and PRC will assess the financial information collected from Country A and to determine ABC as taxable in UK and PRC.

Finding the way forward

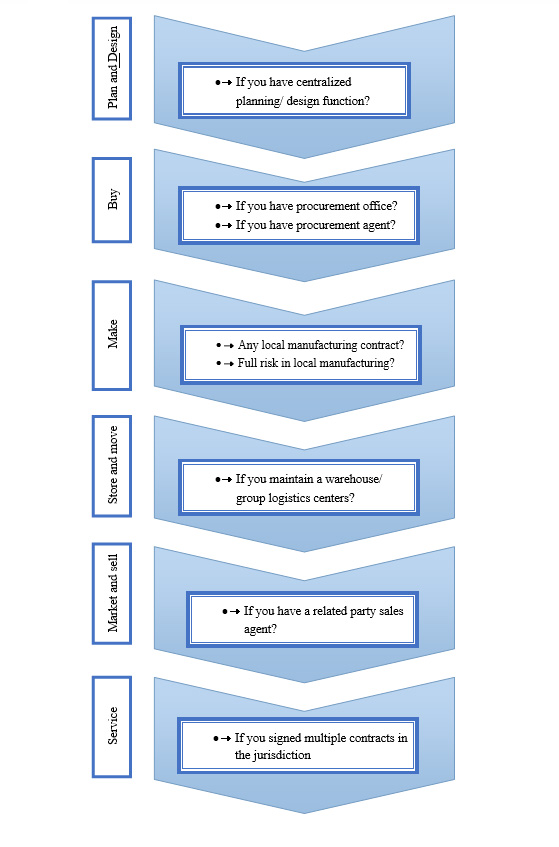

It is a time to rethink your business or operating model to avoid inefficiencies and extra costs, and to allow your company to better navigate a new environment.

Take a look at the entire value chain of your business model associated with BEPS actions, the presence of any below elements can give rise to a taxable presence even though there is no physical office/ company established in a country:

Conclusion

To gain a comparative advantage or to avoid losing your competitiveness in this new world, don’t wait and see. You should have a better management of your tax position in a proactive way, identify potential risk and uncertainties that your current business model is facing, manage tax exposure and develop the most tax-efficient structure for your business.

If you would like to learn more about the impact of BEPS project/ CRS/ CbC reporting/ AEOI, please contact us for advisory service.